🎯 STRisker: Bulletin - Turkey

The 1% accommodation tax rate is the relief effort's first concrete win; licensing requirements and VAT obligations stay put

{kind=link}

Turkey Halves Accommodation Tax Through Year-End

Photo by Anna Berdnik on Unsplash

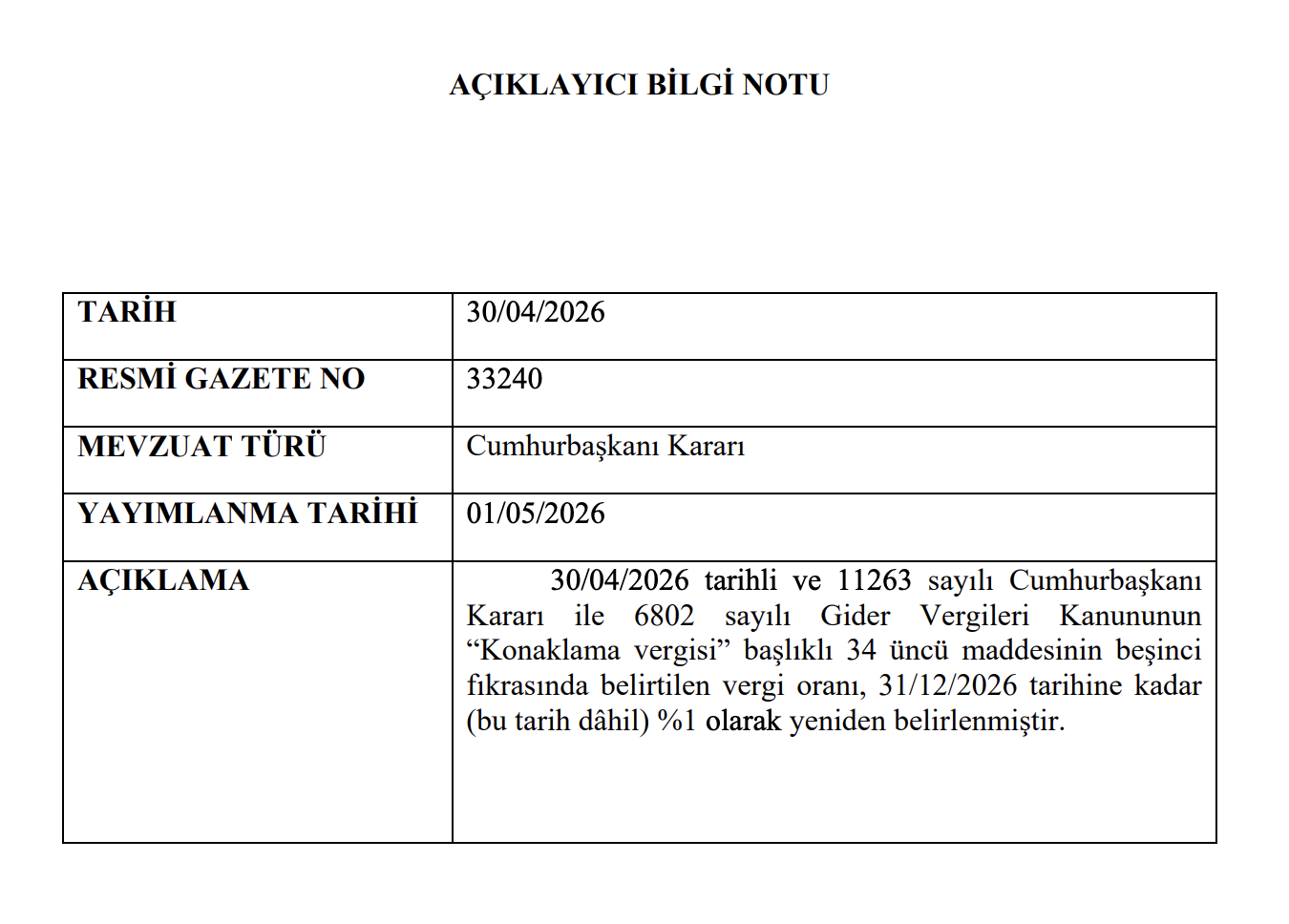

Turkey's Ministry of Culture and Tourism oversees a short-term rental market that just received a modest tax reprieve. The Presidential Decision No. 11263 that was published in the Official Gazette on 30 April 2026 cuts the accommodation tax from 2% to 1% effective 1 May through 31 December 2026. The reduction applies across all accommodation providers including hotels, licensed STR operators and tourism-purpose residential rentals. For hosts navigating the mandatory licensing framework under Law No. 7464, the cut offers a limited but immediate pricing advantage during what industry leaders describe as a period of softening inbound demand.

Dating back to 1 January 2023, the accommodation tax is calculated on revenue excluding VAT and falls squarely on the property owner or operator. Hosts must declare and pay it monthly to the Turkish Revenue Administration regardless of how the booking was made. Under Law No. 7464, any residential property rented for 100 days or fewer requires a Tourism Purpose Rental Permit (Turizm Amaçlı Kiralama İzin Belgesi) from the Ministry and the accommodation tax applies to all qualifying stays within that framework. Presidential Decision No. 11263 leaves everything else intact: permit requirements, building consent rules and the room-rental prohibition are all unchanged.

Turkey's Accommodation Tax Guide

Accommodation Tax Declaration Preparation Guide

Rising security concerns and surging energy costs tied to the US-Israel-Iran conflict have weighed on travel demand across the broader Middle East with Turkey not being insulated from the slowdown and its government framing the tax cut explicitly as a response to those pressures. Erkan Yağcı, president of the Turkish Hoteliers Federation, described it as essential to keeping Turkey competitive in global markets. Müberra Eresin of the Turkish Hoteliers Association went further and proposed that the accommodation tax be restructured as a fixed per-guest fee paid directly by travelers, arguing that approach would make the cost more visible and the market more competitive internationally.

STRisker Updates Tracker

How do you keep up with the regulatory rollercoaster in your market? STRisker's Updates Tracker can be your guide - start tracking latest events as they happen and get access to essential documents as they come in. We know the struggle, which is why we built this product to capture every twist and turn in the regulatory saga so you never miss a beat.

For STR operators, the tax cut means a smaller number on the monthly declaration but not a simpler compliance picture. Since 1 April 2026, Airbnb has required hosts in Turkey to submit a permit certificate number at the listing level. The platform cross-checks each submission against Ministry of Culture and Tourism records and unverified listings are blocked from accepting new bookings.

Sitting alongside that obligation is a still-unresolved legal question of potentially greater consequence. On 18 December 2025 Turkey's Council of State (Danıştay) suspended the Revenue Administration's practice of automatically classifying STR income as commercial profit, drawing a legal line between simple property rental and organized hospitality. Hosts who do not provide hotel-style services such as daily cleaning, meals or reception could see their income reclassified as ordinary rental income which would eliminate a 20% VAT obligation in the process. A final ruling has not been issued, the 1% rate expires 31 December 2026, and no extension has been announced.

☑️ Tax change: Accommodation tax reduced from 2% to 1% on revenue excluding VAT

☑️ Effective period: 1 May 2026 through 31 December 2026

☑️ Authority: Presidential Decision No. 11263, published 30 April 2026; amends Article 34 of the Expenditure Tax Law (Law No. 6802)

☑️ Who is affected: All accommodation providers including STR operators holding Tourism Purpose Rental Permits

☑️ Collection: Declared and paid monthly by the property owner or operator; platforms do not remit on the host's behalf

☑️ Licensing: Law No. 7464 permit requirements unchanged; mandatory for all rentals of 100 days or fewer

☑️ Platform obligation: Airbnb requires permit number at listing level from 1 April 2026; unverified listings cannot accept new bookings

☑️ VAT status: STR income subject to 20% VAT where classified as commercial; Danıştay suspension of automatic commercial classification for individual hosts pending final resolution

☑️ Non-compliance fines: 100,000 TRY per property (first violation); 500,000 TRY (second); up to 1,000,000 TRY (subsequent)

Airbnb Tax Guide 2026 on Short-Term Rental Taxes, VAT, and Accommodation Tax

Stay Updated with STRisker!

STRisker offers tools and features to keep you updated with the Short Term Rental movement (and now Data Centers!) movement across the world.

👍 We’d love your feedback.

We're always looking for ways to improve Bulletins.

Was this one useful to you? Other topics you'd like to see get covered?

✉️ Just reply directly to this email. We read and respond to every message!

-Will McClure

🙋 P.S.

Know someone else who should be reading this Bulletin? Feel free to forward this along. We want to make sure operators and stakeholders are aware of regulatory changes in their area.