🎯 Strisker: Bulletin - Spain

Draft decree unveiled by the Council of Ministers would strip tourist flats of reduced VAT treatment and push the rate for hosts offering hotel-style services from 10% to the standard 21%

Spain Moves to Raise VAT on Short-Term Rentals to 21% in New Housing Decree

Photo by Harrison Fitts on Unsplash

Watch this news coverage on Youtube

Spain's national government has moved to strip short-term rentals of their preferential VAT treatment and confirmed plans to raise the tax on tourist accommodation to the standard 21% rate as part of a broader housing reform package. Government spokesperson Elma Saiz announced the measure last June 29 following a Council of Ministers meeting, calling the coming decree an "ambitious and cross-cutting" response to the country's housing affordability crisis as multiple outlets reported from the post-cabinet press briefing.

BDO Abogados, VAT Newsletter, June 2025

This newsletter reported an earlier bill distinct from the government's recent announcement that would have taxed short-term rentals under 30 nights at 21% in towns over 10,000 residents even without hotel-style services.

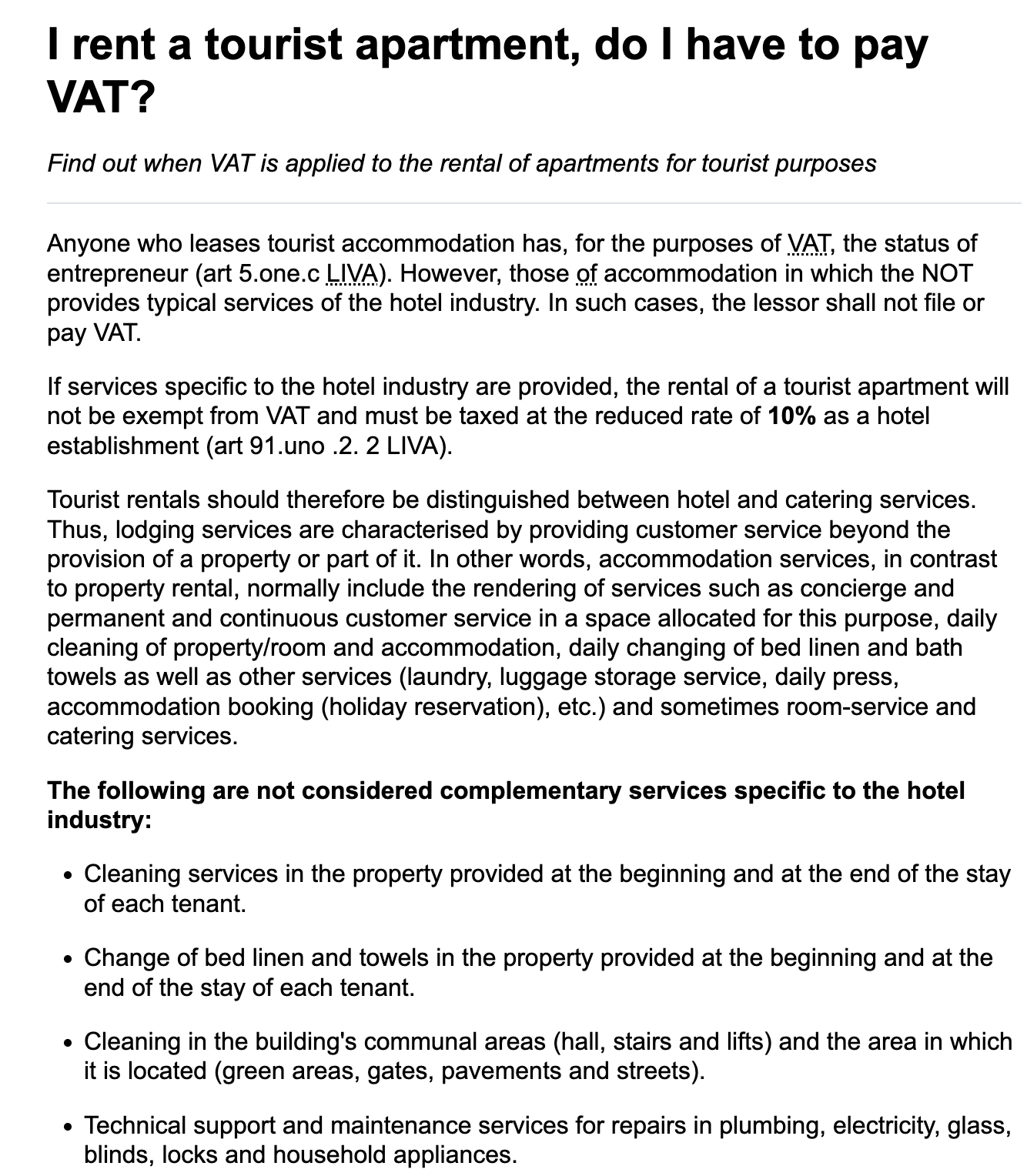

Under current rules, short-term rentals that do not offer hotel-style services such as daily cleaning or reception are generally exempt from VAT while those that do provide such services pay a reduced 10% rate. The draft decree would eliminate that distinction and apply the full 21% rate uniformly to tourist accommodation, a change the Ministry of Housing and Urban Agenda as led by Isabel Rodríguez has framed as a deterrent meant to redirect properties into the long-term residential market. According to Spain's National Statistics Institute (INE), national tourist-housing stock reached roughly 400,000 units at its 2024 peak and stood at 381,837 units as of May 2025 which is roughly 1.4% of the national housing stock.

The VAT increase forms the second of two blocks in the package: the first block targets the long-term rental market directly. It introduces mandatory written contracts for seasonal and room rentals, extends leases expiring before the end of 2027 on an extraordinary basis, and offers income tax incentives to landlords who lower rents voluntarily. The government intends to present the full text to the Congress of Deputies during July to seek cross-party backing broad enough to survive a floor vote which is the bar the coalition failed to clear on April 28 when Congress voted 177 to 166 to reject a separate rental-extension decree Real Decreto-ley 8/2026. Coverage of the debate noted that roughly three million tenants lost the extension as a result.

Ley 37/1992, de 28 de diciembre, del Impuesto sobre el Valor Añadido (Spain's VAT Law)

Articles 20.1.23 and 91.1.2.2 would be amended to apply the 21% rate to tourist rentals which is the specific legal mechanism behind the second block of the government's housing package.

"The exemption shall not apply to the rental of furnished apartments or dwellings where the landlord undertakes to provide complementary services typical of the hotel industry, such as restaurant services, cleaning, laundry, or other similar services."

- Spain's VAT Law (Ley 37/1992), Article 20.1.23

No effective date, formal decree text, or published rate schedule exists yet and the measure remains a policy announcement. Its VAT provisions could also still be amended or dropped during negotiations with the parliamentary groups whose votes the government needs. Airbnb, which already collects and remits 21% VAT on its own service fees for Spanish bookings, would likely need to update host-facing tax guidance once the accommodation-side rate is finalized though no platform-specific obligations yet have been detailed in the current proposal.

⦾ Effective date: Not yet set; decree is targeted for presentation to Congress in July 2026; no gazette date exists.

⦾ Registration required: No change from existing rules under this proposal.

⦾ Night cap: N/A. This is a tax change, not an occupancy or licensing restriction.

⦾ VAT change: From exempt/10% (reduced rate for hosts offering hotel-style services) to a flat 21% for tourist accommodation.

⦾ Penalty for non-compliance: Not yet specified; standard Spanish VAT enforcement provisions would apply once in force.

⦾ Platform responsibility: Not yet detailed for accommodation VAT; platforms already remit VAT on their own service fees.

In case you missed it:

Strisker Document Analysis

Finding the right compliance documents shouldn’t feel like searching for a needle in a haystack - Strisker’s Documents Analysis is built to simplify your life, offering instant access to hundreds of thousands of documents from thousands of cities across the world.

Stay Updated with STRisker!

STRisker offers tools and features to keep you updated with the Short Term Rental movement (and now Data Centers!) movement across the world.

👍 We’d love your feedback.

We're always looking for ways to improve Bulletins.

Was this one useful to you? Other topics you'd like to see get covered?

✉️ Just reply directly to this email. We read and respond to every message!

-Will McClure

🙋 P.S.

Know someone else who should be reading this Bulletin? Feel free to forward this along. We want to make sure operators and stakeholders are aware of regulatory changes in their area.